Health insurance is a financial product that provides coverage for medical and surgical expenses incurred by individuals or groups. It is designed to protect individuals and families from the high costs of healthcare services and treatments. Health insurance plans vary in terms of coverage, costs, and the specific medical services they include.

Definition of Health Insurance:

Health insurance is a contract between an individual or a group and an insurance company or a government program. It involves the payment of regular premiums in exchange for the insurer assuming the financial risk of covering medical expenses. In other words, health insurance provides a mechanism for pooling and distributing the financial risks associated with healthcare, allowing individuals to access medical services without bearing the full burden of the costs.

Health insurance typically covers a wide range of medical services, including preventive care, diagnostic tests, hospitalization, surgeries, medications, and sometimes even dental and vision care. The specific coverage and benefits of a health insurance plan depend on the type of plan, the insurance provider, and the terms of the policy.

Health insurance plans can be obtained through various sources, including employers, government programs (such as Medicare and Medicaid), and individual marketplaces. Employer-sponsored health insurance is a common form of coverage, where employers offer health insurance benefits to their employees as part of their overall compensation package.

Health insurance operates on the principle of risk sharing. The premiums paid by policyholders collectively form a pool of funds that the insurer uses to cover the medical expenses of those who require healthcare services. This system allows individuals to have access to necessary medical care while reducing the financial burden on individuals and promoting affordability.

It is important to note that health insurance plans often have deductibles, copayments, and coinsurance. Deductibles refer to the amount individuals must pay out of pocket before the insurance coverage kicks in. Copayments are fixed amounts paid by individuals at the time of receiving medical services, while coinsurance is a percentage of the medical costs that individuals are responsible for after meeting their deductible.

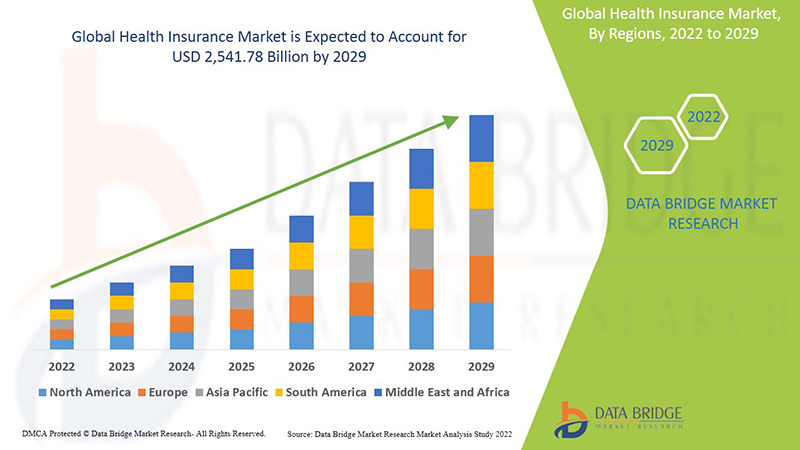

Health Insurance Market Size

- The demand for health insurance is on the rise due to several factors, including increasing costs for medical services and the growing number of day care procedures. As a result, the health insurance market is projected to reach a value of USD 2,541.78 Billion by the year 2029, with a compound annual growth rate (CAGR) of 4.6% during the forecast period. The “Corporates” segment represents the most prominent end-user segment in this market, driven by the growing demand for group health insurance by corporations.

- The market report provided by Data Bridge Market Research offers comprehensive insights into the health insurance market. The report includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and a climate chain scenario. These analyses provide a thorough understanding of market dynamics, including market trends, key players, market size, and growth potential.

- The rising costs of healthcare services have made health insurance a crucial financial product for individuals and organizations alike. With the support of health insurance, individuals can access necessary medical care without facing the full burden of the expenses. Corporations recognize the importance of providing group health insurance to their employees, as it helps attract and retain talent while ensuring the well-being and productivity of their workforce.

- The findings from Data Bridge Market Research highlight the significant growth potential in the health insurance market. The projected CAGR indicates a steady increase in the adoption of health insurance, driven by the need for financial protection against escalating healthcare costs. The comprehensive market report provided by Data Bridge Market Research equips stakeholders with valuable insights and analysis to make informed decisions and capitalize on the opportunities in this expanding market.

Types of Health Insurance Plans

- When it comes to health insurance, understanding the different types of plans available is crucial for selecting the right coverage that meets your healthcare needs. Here are some common types of health insurance plans:

- Health Maintenance Organization (HMO) Plans: HMO plans typically have a network of healthcare providers that policyholders must choose from. They require individuals to select a primary care physician (PCP) who serves as a gatekeeper for referrals to specialists. HMOs generally offer comprehensive coverage but require individuals to stay within the network for non-emergency services.

- Preferred Provider Organization (PPO) Plans: PPO plans offer more flexibility than HMOs. They have a network of preferred providers, but individuals can seek care outside the network, although at a higher cost. PPO plans generally don’t require a PCP or referrals for specialist visits, providing greater autonomy in choosing healthcare providers.

- Exclusive Provider Organization (EPO) Plans: EPO plans are a mix between HMO and PPO plans. They have a network of providers like an HMO, but individuals are not required to choose a PCP or get referrals for specialists. However, similar to HMOs, EPO plans may not cover out-of-network services, except in emergencies.

- Point of Service (POS) Plans: POS plans combine elements of HMO and PPO plans. Like an HMO, individuals choose a PCP and need referrals for specialists within the network. However, individuals can also seek care outside the network, albeit with higher out-of-pocket costs.

- High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs): HDHPs have lower monthly premiums but higher deductibles compared to other plans. They are often paired with HSAs, which allow individuals to save pre-tax money for qualified medical expenses. HDHPs with HSAs are suitable for individuals who are generally healthy and prefer lower premiums but want to save for future medical costs.

- Catastrophic Health Insurance Plans: Catastrophic plans are designed for individuals under 30 or those who qualify for a hardship exemption. They have low monthly premiums but high deductibles. Catastrophic plans provide coverage for essential health benefits after the deductible is met, protecting individuals from major medical expenses.

For more information about health insurance market visit

https://www.databridgemarketresearch.com/reports/global-health-insurance-market

About data bridge market research

Market research studies from all over the world are made available in the Data Bridge Market Research library. Pre-packaged syndication The most pertinent business intelligence may be found with the aid of market research investigations.

For both large and small firms, our research analyst offers market research studies and business insights.

The firm aids clients in developing and growing market-specific business strategies. Data Bridge Market Research is interested in learning about your business, country profiles, industry trends, facts, and analysis. These sectors include FMCG, Agriculture, Telecommunications, Healthcare, Pharmaceuticals, Chemical, ICT, etc.